Religion

Religion

Religion

Religion  Crime

Crime 10 Infamous Crime Scenes That Became Tourist Hotspots

Our World

Our World 10 Rare Hybrids with Wild Backstories

Space

Space 10 Amazing Explanations for Cosmic Conundrums

Movies and TV

Movies and TV 10 Film Productions That Went Too Far

Weird Stuff

Weird Stuff 10 Historical Facts That Ruin Your Timeline

History

History 10 Maritime Folktales with a Real-Life Twist

Crime

Crime 10 Notorious Prison Gangs That Became Criminal Empires

Music

Music Top 10 Hit Song Lyrics That Became Cultural Catchphrases

Weird Stuff

Weird Stuff 10 Bizarre Viral Trends That Took Things Too Far

Religion 10 Forgotten Greek Gods Beyond Olympus

Crime 10 Infamous Crime Scenes That Became Tourist Hotspots

Our World 10 Rare Hybrids with Wild Backstories

Who's Behind Listverse?

Jamie Frater

Head Editor

Jamie founded Listverse due to an insatiable desire to share fascinating, obscure, and bizarre facts. He has been a guest speaker on numerous national radio and television stations and is a five time published author.

More About Us

Space 10 Amazing Explanations for Cosmic Conundrums

Movies and TV 10 Film Productions That Went Too Far

Weird Stuff 10 Historical Facts That Ruin Your Timeline

History 10 Maritime Folktales with a Real-Life Twist

Crime 10 Notorious Prison Gangs That Became Criminal Empires

Music Top 10 Hit Song Lyrics That Became Cultural Catchphrases

Weird Stuff 10 Bizarre Viral Trends That Took Things Too Far

Top 10 Intriguing Facts About Bitcoin

Since the start of the Internet age, businesses have used this worldwide platform to sell their products to an ever-increasing share of the world’s populace. Most of us have bought items off the Internet using credit cards or bank accounts. But over the years, developers have tried to find a way to create a unique currency just for the digital marketplace. In 2009, they did with the introduction of Bitcoin.

10 The First Bitcoin Transaction Was For Pizza

On May 18, 2010, Laszlo Hanyecz posted on a forum for Bitcoin: Bitcoin Talk. At the time, Bitcoin was still in its infancy. It was incredibly volatile, and each Bitcoin was worth only a few pennies on the dollar. Hanyecz’s post was for two Papa John’s pizzas that he said he would pay 10,000 bitcoins for. This transaction would go down in Internet history as the first time that Bitcoins were actually used to buy something.

On May 22, Hanyecz posted that someone had taken him up on the offer. At the time, he just thought it was cool that he could get pizza for seemingly nothing. Hanyecz continued to buy pizza with Bitcoins until the summer when he ran out of Bitcoins. He didn’t give any of this a second thought because he believed—as many others did at the time—that Bitcoin was never going to actually go anywhere as an Internet currency.

For the next few years, it seemed that what everyone thought about Bitcoin was true. But in 2013, investors and speculators became interested in Bitcoin and began to trade it on a much larger scale. Soon, the value of Bitcoin began to skyrocket as it became a popular commodity. In the coming months, one Bitcoin went from being valued at a few pennies to $1,200. It finally settled between $500 and $700. If Hanyecz had spent 10,000 Bitcoins in mid-2014 on two pizzas, they would have been worth around $5 million.

9 Bitcoin’s First Major Use Was On The Silk Road

Photo credit: Federal Bureau of Investigation

For those unaware of the Silk Road, it served as a way for anonymous Internet buyers to order illegal drugs. Named after the famed trade route between Europe and the Orient, it operated clandestinely from its conception until it was taken down in 2013 after an intensive investigation by various government agencies. One of the keys to the Silk Road’s success was the use of a completely anonymous form of payment: Bitcoin.

Due to the nature of its operations, the Silk Road could only be accessed through the Tor anonymizing network. Once you entered the Silk Road, you could buy drugs from cocaine to LSD along with other items like fake IDs, stolen credit card numbers, and hacking tools.

Law enforcement couldn’t penetrate the Silk Road because of its savvy users. The Tor network blocked out any digital identification, and the use of Bitcoins only led to certain IP addresses which provided little to no real information. To finally take down the seemingly invulnerable Silk Road, a multi-organization task force, dubbed “Marco Polo” after the famed explorer of the Silk Road, was created with the cooperation of the FBI, DHS, IRS, DEA, US Postal Service, and the Department of Alcohol, Firearms, and Tobacco.

Their target was a mysterious figure known as the Dread Pirate Roberts, the founder and operator of the Silk Road. This was the first time that government agencies had become involved with such intricate digital technology, so they were mostly in the dark as to how they would deal with the Silk Road.

They began by making a series of arrests of various sellers and gathered information bit by bit about the inner functioning of the organization. It wasn’t until 2013 that the Dread Pirate Roberts (aka Ross Ulbricht) was caught. This episode taught a valuable lesson as to how easy it could be to operate anonymous illegal operations digitally with the use of tools like Bitcoin.

8 Bitcoins Have Created An Entire ‘Mining’ Industry

Photo credit: Marco Krohn

Bitcoin “mines” are where complex algorithms are solved and Bitcoins themselves are generated. The majority of these mines are located in China where they are often hidden facilities that operate outside the law. As a result, the operations have to be highly secretive. The Chinese government has not issued a policy for or against Bitcoins, so for the time being, they have been used to generate fortunes for their miners.

One facility called Bitbank, which is operated by entrepreneur Chandler Guo, has generated $8 million a year and is considered one of the largest mines in the country. Workers at the facility solve cryptographic problems on computers to authenticate transactions around the world. Each transaction that is solved adds a “block” to the “block chain,” and those who solve the problems receive Bitcoins in return.

At the Bitbank facility, around 50 Bitcoins are generated each day by workers who operate 24 hours a day. At one time, China only had around 40 percent of the world’s Bitcoin mines, but by 2016, it controlled the lion’s share with nearly 70 percent of all mines located in the country.

Not all of those in the Bitcoin community are happy about this. Enthusiast Michael Hearn says that the slow Internet in China will weigh down the popularity of Bitcoins and lead to a possible failure of the currency.

7 Bitcoins Are Incredibly Easy To Steal

In 2014, the world’s largest Bitcoin exchange, Mt. Gox, filed for bankruptcy after claiming that around 850,000 Bitcoins were stolen by hackers. At the time, the stolen Bitcoins were worth $450 million. Mark Karpeles, the CEO of Mt. Gox, claimed that $27 million in cash was also stolen. This sent troubling shock waves through the community because it exposed how easy it was to steal Bitcoins with very little effort.

With a fair knowledge of hacking, one can easily access Bitcoin exchanges, which was exactly what the still-unknown perpetrators did. Mt. Gox had long been the target of hackers, with 80,000 Bitcoins stolen by hackers before Karpeles took over the company in 2011.

It is known that Karpeles embezzled $2.7 million from the company, but 650,000 Bitcoins (around $300 million) are still unaccounted for. It’s not just exchanges that are being hacked, either.

Sheep Marketplace, one of the successors to Silk Road, was the victim of a £60 million heist that caused the site to fall apart soon afterward. Apparently, the hackers were able to fake balances in people’s accounts until they managed to wipe the site clean within a week.

Since Bitcoins don’t actually disappear, they have to be laundered in a different manner than actual currency. They are slowly tumbled down block chains and mixed with other Bitcoins until all the stolen ones have disappeared.

As the process can actually be tracked, many Sheep Marketplace users managed to find where their Bitcoins were being tumbled. In 2016, two men from Florida were found to have committed the heist, but by then, the value of their Bitcoins was only $6.6 million.

6 Bitcoins Are Currency For Extortionist Hackers

In February 2016, Hollywood Presbyterian Medical Hospital was hacked and its system held for ransom. With its system being held by hackers, none of the operations could be moved forward. With lives on the line, the hospital could do nothing but comply with the hackers demands: $17,000 in Bitcoins. The crime was despicable, but it isn’t an isolated occurrence.

Before the hospital hack, there had been other incidents of extortion but for considerably smaller sums. For example, a police department in Boston paid $500 in Bitcoins to extortionists and a sheriff’s department in Maine made a similar payment.

Although the extortionists have not been identified yet, it is known that one network based in either Russia or Ukraine has generated almost $16.5 million in Bitcoin income from hacking victims in the United States. The extortion payments are usually in the amount of $20,000 and always in Bitcoin.

Since Bitcoin wallets don’t have to be registered with any government, it has become the most popular currency for digital extortionists. One group known as DD4BC has recently become well-known among corporations for demanding $10,000 in Bitcoins.

One email from DD4BC that was made public reads: “Do not ignore me, as it will just increase the price. [ . . . ] Once you pay me, you are free from me for the lifetime of your site.” Although various digital security sources have offered some solutions—like digitally marking the Bitcoins that are used (similar to how stolen bills are tracked)—the extortion has continued.

5 Bitcoins Allow For Easy Scamming

Keeping in mind all the other crimes that can be enabled by Bitcoins, one can assume that scammers would naturally take to crypto urgency. According to a 2015 report, Southern Methodist University identified several of the most common scams involving Bitcoins. From 2011 to 2014, 41 different scams occurred with a total take of nearly $11 million.

Bitcoin investment scams are fairly simple and are similar to Ponzi schemes. Investors are told that they can receive unreasonably high yields, but ultimately, they are just dumping money into the scammer’s wallet.

For example, with fake Bitcoin mines, scammers claim to be mining Bitcoins for you for a fee but are in fact just pocketing the fee. There are also Bitcoin wallet scams in which you are seemingly depositing your money into a verified Bitcoin wallet, but all the funds are actually transferred to the scammers at a certain point. The last scam is a Bitcoin exchange in which low exchange rates from turning Bitcoins into currency are offered, but the scammers never deliver on their side of the exchange.

Disturbingly enough, a scam emerged from the June 2016 mass shooting tragedy in Orlando in which scammers put up a Twitter account claiming to be the club Pulse where the shooting occurred. The account took Bitcoin donations. Since the donations couldn’t be tracked, the scammers tried to profit from the tragedy and well-meaning people.

Luckily, most Twitter users who followed the donation link provided by the account realized immediately that the page they were taken to was unrelated to Pulse because the domain used was only six months old and there were blatant spelling errors. The scam only took in $30 before being taken down.

4 Bitcoins Could Be Used For Terrorist Purposes

Photo credit: Day Donaldson

In 2014, someone using the name Amreeki (“American”) Witness posted a .pdf on WordPress in which he stated that it was hard for most supporters of ISIS to give money due to restrictions by the ruling government of Iraq. His remedy was to have supporters donate Bitcoins which, of course, couldn’t be tracked if the process of “mixing” the currency was used.

Bitcoins could be a possible game changer for terrorism funding because of the anonymity afforded by the currency. While it can be tracked somewhat, the currency can be effectively laundered (through enough “mixing”) to any illicit group like ISIS. While groups like ISIS would still need real currency to continue operating, the Pentagon has named digital currencies like Bitcoin as a possible threat because they could be a possible source of revenue for terrorists.

After the 2016 Paris attacks, however, the European Union began to crack down on possible terrorist financing. Their first target was financing through Bitcoin. The European Commission, the financial arm of the EU, is considering adding regulations to Bitcoin in which there has to be an identity attached to the Bitcoins to prevent them from going to terrorist groups.

Like the Silk Road, the deep web is the preferred domain of ISIS, and this is where Bitcoins from sympathizers go. Although removing the anonymity of Bitcoins would change one of its key aspects, most Bitcoin users and exchanges would not mind the changes because most Bitcoins are used for legitimate purposes.

3 The Creator Of Bitcoin Is A Mystery

All that is known about the creator of Bitcoin is that he went by the name Satoshi Nakamoto. Like the currency he invented, Satoshi is almost completely anonymous. As it goes, he introduced the currency in 2009 and communicated with the first users by email—never by phone or in person. Even after the spectacular rise of Bitcoin, Satoshi continued to remain in the shadows and disappeared completely in 2011.

In 2014, Newsweek ran a cover story claiming to have discovered Satoshi. They stated that Satoshi was a unemployed engineer in his sixties living in a Los Angeles suburb. Those involved with Bitcoin made it clear that he was not Satoshi.

Another theory believed by many in the Bitcoin community is that Satoshi is actually a reclusive American man of Hungarian descent named Nick Szabo. However, Szabo denies that he is Satoshi, although he remains one of the key figures in Bitcoin.

Satoshi hasn’t been involved with Bitcoin since 2011, so his presence really doesn’t matter in the grand scheme of things. But there are still some who speculate about his identity.

In May 2016, an Australian entrepreneur named Craig Steven Wright claimed to be Satoshi, but skeptics immediately said that he was not the real Satoshi and that if the real Satoshi wished to be known, there would be no doubt as to his identity. Those who believe Wright say that it doesn’t matter either way as Bitcoin would go on with or without him.

Whatever the case, at the time Satoshi left, he had as many as one million Bitcoins, which could easily be worth in the hundreds of millions of dollars today.

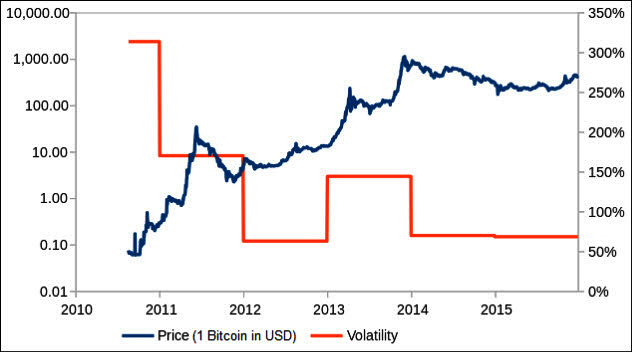

2 Bitcoins Are Incredibly Volatile For Many Reasons

Photo credit: Ladislav

Since Bitcoins were first launched, the price has gone from pennies on the dollar to several hundreds of dollars as of mid-2016. However, even though the price is far higher in 2016 than it once was, it still fluctuates and remains quite volatile. For this reason, many people still have reservations about the currency. Over the years, many have also come up with reasons why the price can both fall and rise spectacularly.

Bitcoins follow the economic principle of supply and demand, and the course of their price can be determined by this. In 2014, the price fell by 60 percent and many took this as a sign that Bitcoin might finally die out.

That year, though, several Silicon Valley companies started to invest in Bitcoins. In addition, various other companies began accepting Bitcoins as a form of payment, which caused the currency’s value to rise once again. Although it may not have taken off as a common currency among average people, its technical innovations continued to allow it to prosper.

In 2015, Bitcoins again became volatile because of an apparent Russian pyramid scheme which became incredibly popular in China. As Bitcoin was the only currency taken in the Russian scheme, the Chinese began to buy in droves, causing the price to rise.

This year, Chinese demand again drove up the price of Bitcoins when the yuan was devalued. This caused prices to go up by 20 percent. Although prices continue to fluctuate, experts agree that Bitcoins will mostly likely remain on the market for some time—as long as more companies adopt them as a form of payment and demand remains in place.

1 Bitcoins Might Collapse In The Future

Photo credit: fdecomite

As mentioned earlier, Bitcoin enthusiast Mike Hearn believes that Bitcoins might fail in the future if they continue to follow their current path. According to Hearn, those in control of Bitcoin have lost track of the original purpose of the currency. Many discredited Hearn, but his prophecy has caused some to look deeply into Bitcoin’s functions and the reasons why he claimed Bitcoins are doomed.

His first reason was that Bitcoins were initially meant to be a decentralized currency, unlike most other physical currencies. However, Bitcoins are now controlled by a small group of people, the exact opposite of what was supposed to happen.

Hearn also claimed that there is an internal split at Bitcoin between those who want technology to increase transactions and those who are opposed to this. Blockchain, the technology behind the Bitcoin transactions, has become increasingly random as to the speed of transactions. Hearn said that it could take anywhere from 60 minutes to 14 hours for a transaction to go through.

However, his main issue was with the small number of people (approximately 10) in control of Bitcoin. As long as it is controlled by this small number, he said, Bitcoin will be an “inescapable failure.” We don’t know whether Hearn will be proved right, but as it stands, Bitcoin has become one of the most interesting phenomena of the Internet age.

More Great Lists

Top 10 Bizarre Facts About Bitcoin

Top 10 Bizarre Facts About Bitcoin Top 10 Intriguing Facts Involving Iron

Top 10 Intriguing Facts Involving Iron 10 Intriguing Facts You Need To Know About Golems

10 Intriguing Facts You Need To Know About Golems 10 Religious Places With Intriguing Facts And Fakes

10 Religious Places With Intriguing Facts And Fakes 10 Intriguing Facts About The Manhunt For John Wilkes Booth

10 Intriguing Facts About The Manhunt For John Wilkes Booth Top 10 Intriguing Things That Make Ice Incredible

Top 10 Intriguing Things That Make Ice Incredible Top 10 Intriguing Cases Involving Art About Jesus

Top 10 Intriguing Cases Involving Art About Jesus 10 Most Intriguing Atmospheric Events That Could…

10 Most Intriguing Atmospheric Events That Could… 10 Intriguing Cases Involving Rare Ancient Art And Writing

10 Intriguing Cases Involving Rare Ancient Art And Writing

fact checked by

Jamie Frater

More Great Lists